While global and Australian shares had a nice bounce from their late October lows – rallying about 5%, partly reversing their 10% or so top to bottom fall, they have since fallen back to their lows as the worries about US rates, bond yields, trade, tech stocks, etc, have morphed into broader concerns about global growth and profits. Fears of a credit crunch and falling home prices are probably not helping Australian shares either, which this week dipped below their October low. Our assessment remains that it’s too early to say we have seen the lows, but we remain of the view that it’s not the start of major bear market.

The three bears – correction, gummy & grizzly

Very simply there are 3 types of significant share market falls:

-

corrections with falls around 10% (of course these aren’t really bear markets – but some might feel that they are!);

-

“gummy” bear markets with falls around 20% meeting the technical definition many apply for a bear market but where a year after falling 20% the market is up (like in 1998 in the US, 2011 and 2015-16 for Australian & global shares); and

-

“grizzly” bear markets where falls are a lot deeper and usually longer lived (like in 1973-74, US and global shares through the tech wreck or the GFC).

I can’t claim the terms “gummy bear” and “grizzly bear” as I first saw them applied by stockbroker Credit Suisse a few years ago. But they are a good way to conceptualise them. Grizzly bears maul investors but gummy bears eventually leave a nicer taste (like the lollies). Corrections are quite normal and healthy as they enable the sharemarket to let off steam and not get too overheated. As can be seen in the next chart, excluding the present episode since 2012 there have been four corrections and one gummy bear market (2015-16) in global and Australian shares. Bear markets generally are a lot less common, but arguably what we saw in 2015-16 was a gummy bear market.

Source: Bloomberg, AMP Capital

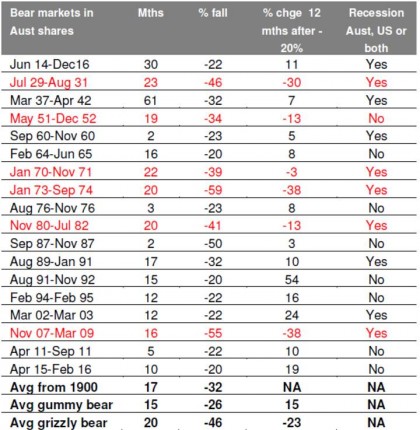

The next table shows conventionally defined bear markets in Australian shares since 1900 – where a bear market is a 20% decline that is not fully reversed within 12 months. The first column shows bear markets, the second shows the duration of their falls and the third shows the size of the falls. The fourth shows the percentage change in share prices 12 months after the initial 20% decline. The final column shows whether they are associated with a recession in the US, Australia or both.

Bear markets in Australian shares since 1900

Based on the All Ords, excepting the ASX 200 for 2015-16. I have defined a bear market as a 20% or greater fall in shares that is not fully reversed within 12 months. Source: Global Financial Data, Bloomberg, AMP Capital

If a gummy bear market is defined by a 20% decline after which the market is higher 12 months later whereas as grizzly bear market sees a continuing decline over the subsequent 12 months after the first 20% decline, then since 1900 there have been 12 gummy bear markets (these are highlighted in black) and there have been six grizzly bear markets (highlighted in red). Several points stand out. First, the gummy bear markets tend to be a bit shorter and see much smaller declines averaging 26% compared to 46% for the grizzly bear markets.

Second, the average rally over 12 months after the initial 20% fall is 15% for the gummy bear markets but it’s a 23% decline for the grizzly bear markets.

Finally, and perhaps most importantly the deeper grizzly bear markets are invariably associated with recession, whereas the milder gummy bear markets including the 1987 share market crash tend not to be. Five of the six grizzly bear markets saw either a US or Australian recession or both whereas less than half of the gummy bear markets saw recession.

It’s also the case that US share market falls are much deeper and longer when there is a US recession.

What’s it likely to be this time?

Our view remains that a grizzly bear market is unlikely because, short of some unforeseeable external shock, a US, global or Australian recession is not imminent. In relation to the US:

-

Business and consumer confidence are very high.

-

While US monetary conditions have tightened they are not tight and they are still very easy globally and in Australia (with monetary tightening still a fair way off in Europe, Japan and Australia). We are a long way from the sort of monetary tightening that leads into recession.

-

Fiscal stimulus is continuing to boost US growth.

-

We have not seen the excesses – in terms of debt growth, overinvestment, capacity constraints and inflation – that normally precede recessions in the US, globally or Australia.

Reflecting this, global earnings growth is likely to remain reasonable – albeit slower than it has been – providing underlying support for shares. In relation to Australia – yes housing is turning down and this will weigh on consumer spending, but it will be offset by a lessening drag from mining investment, strengthening non-mining investment, booming infrastructure spending and solid growth in export earnings. Growth is unlikely to be as strong as the RBA is assuming but it’s unlikely to slide into recession either.

So, for all these reasons it’s unlikely the current pull back in shares is the start of a grizzly bear market. However, we have already had a correction in mainstream global shares and Australian shares (with circa 10% falls) and with markets falling again it could turn into gummy bear market, where markets have another 10% or so leg down – a lot of technical damage was done by the October fall that has left investors nervous, the rebound from late October was not particularly convincing and many of the drivers of the October fall are yet to be resolved.

Some positives

However, there are three developments that help add to our conviction that we are not going into a grizzly bear market. First, recent comments by Fed Chair Powell and Vice Chair Clarida indicate that the Fed remains upbeat on the US economy and a December hike looks assured (for now), but it is aware of the risks to US growth from slowing global growth, declining fiscal stimulus next year, the lagged impact of eight interest rate hikes and stock market volatility and appears open to slowing the pace of interest rate hikes or pausing at some point next year. The stabilisation in core inflation around 2% seen lately may support this. Past gummy bear markets (1987, 1998, 2011, 2015-16) all saw some pause or relaxation by the Fed.

Second, while it’s messy after the US/China standoff at the recent APEC forum there have been some positive signs on trade. Talks between the US and China on trade have reportedly resumed ahead of a meeting between President Trump and President Xi at the G20 summit next week and President Trump has repeated that he is optimistic of a trade deal with China and that the US might put any further tariff increases on China on hold if there is progress. The US/China trade dispute is unlikely to be resolved quickly when Trump and Xi meet. Perhaps the best that can be hoped for is agreement to have formal trade talks with the aim of resolving the issues and the US agreeing to delay any further tariff increases. With Trump wanting to get re-elected I remain of the view that some sort of deal will be agreed before the tariffs cause too much damage to the US economy. Rising unemployment (as fiscal stimulus will turn to contraction next year if current and proposed tariffs/taxes on China go ahead) and higher prices at Walmart will sink Trump’s re-election prospects in 2020. Of course, investors are now highly sceptical of any progress on the trade front. So any breakthrough in the next six months could be a big positive.

Finally, while the 30% plunge in the oil price since its October high is a short-term negative for share markets via energy producers, it has the potential to extend the economic cycle as the 2014-16 oil price plunge did. The main drivers of the fall in the oil price are slower global demand growth, US waivers on Iranian sanctions allowing various countries to continue importing Iranian oil, rising US inventories, the rising $US and the cutting of long oil positions. While oil prices are unlikely to fall as much as in 2014-16 when they fell 75% (as OPEC spare capacity is less now) they may stay lower for longer. This is bad for energy companies but maybe not as bad for shale producers as in 2015 as they are now less indebted and their break-even oil price has already been pushed down to $50/barrel or less. It will depress headline inflation (monthly US inflation could be zero in November and December) and if oil stays down long enough it could dampen underlying inflation. All of which may keep rates lower for longer. And its good news for motorists who see rising spending power. For example, Australian petrol prices have plunged from over $1.60 a litre a few weeks ago to below $1.30 in some cities. That’s a saving in the average weekly household petrol bill of around $10.

Source: Bloomberg, MotorMouth, AMP Capital

Source: AMP Capital 22 November 2018

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.