For some time now, the investment world has been characterised by a search for decent yield paying investments. This “search for yield” actually started last decade but was interrupted by the Global Financial Crisis (GFC) and the Eurozone debt crisis before resuming again in earnest.

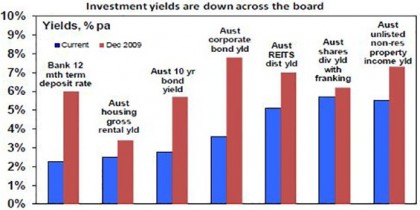

When investment assets are in strong demand from investors, their price goes up relative to the cash flow (eg dividends, interest or rent) they provide pushing their yield down. This is evident in recent times in response to the “search for yield” with yields falling across the board as the next chart shows.

Source: Bloomberg, REIA, RBA, AMP Capital

But everything goes in cycles. So has the “search for yield” gone too far? Will the US Federal Reserve’s shift to start reducing its bond holdings cause a reversal?

Drivers of the search for yield

Interest in yield based investing is not new and is in fact a normal part of investing. Particularly when investors are a bit wary about going for growth. In fact, in Japan it’s become pretty much the norm as interest rates have been stuck at zero for years. In the 1950s, yield focussed investing was the norm in the US and Australia. The search for yield also became apparent last decade and played a role in the GFC itself (as investors piled into yield based investments underpinned by “sub-prime” mortgages, oblivious of the risks). There are three main drivers of the “search for yield” in recent years:

-

First, low interest rates and bond yields and the flow on to bank deposit rates due to low inflation and sub-par growth have encouraged investors to search for higher yielding investments. Central banks buying up bonds and displacing investors into other assets have accentuated this.

-

Second, reduced fear of economic meltdown (as the GFC and subsequently the Eurozone public debt crisis subsided) has helped investors feel comfortable in taking on the greater risk that this entails.

-

Finally, aging populations in developed countries is seeing baby boomers move into pre-retirement and retirement, driving a demand for less volatile investments paying income. Normally, this demand would go to bonds and bank deposits but as their yields are so low some of this demand has gone into other yield paying investments.

Demand for yield from aging populations has further to go as populations age. For example, in Australia the share of the population aged 65 and over is projected to rise from 15% now to 22% by 2061. However, the second driver is cyclical and will reverse next time there is a sustained bout of risk aversion – just as it did in the GFC.

The first driver is a mix of structural and cyclical influences, though, and it’s probably been the main driver of the search for yield. Bond yields and interest rates have been trending down for 30 years or so and this is structural reflecting a downtrend in inflation, which resulted in a long-term super cycle bull market in bonds. But falls this decade also contain a big cyclical element reflecting the sub-par global growth and deflation seen after the GFC. This accentuated the super cycle bull market in bonds and put the search for yield on steroids. This is where the greatest risk of a reversal in the search for yield trade lies.

The logic of falling yields

The search for yield is understandable and can be seen in relation to Australian commercial property ie office, retail and industrial property. The next chart shows average commercial property yields and 10-year bond yields. While average commercial property yields have fallen since the early 1980s from an average of 8.3% to around 5.5%, the yield on bonds has crashed. The longer the decline in bond yields has persisted, the more investors have expected it to continue, driving rising demand for higher yielding assets like property.

Source: Bloomberg, AMP Capital

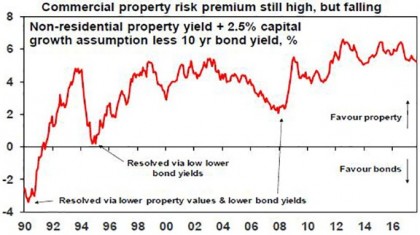

With Australian 10-year bonds yielding 2.8%, it’s little wonder investors might find commercial property on an average yield of around 5.5% more attractive particularly once capital growth of, say, 2.5% pa (ie inflation) for a total return of 8%, is allowed for. The property risk premium – the return potential property provides over bonds – at 5.2% remains high & well above early 1990s and pre-GFC levels that caused problems for property.

Source: Bloomberg, AMP Capital

The same logic applies to investment in assets such as unlisted infrastructure, listed variants of both commercial property and infrastructure, shares and corporate debt.

But are we getting close to a reversal?

Has it gone too far? The greatest risks are around corporate debt where the gap between US investment grade and junk bond yields and US government bond yields has narrowed sharply to around levels that prevailed prior to the tech wreck and again prior to the GFC. But as we saw in the mid-1990s and mid-2000s, spreads can remain low for a while before trouble arises, which is usually when the economy turns down and there is no sign of that just yet.

For equities the gap between the forward earnings yield on shares and bond yields has narrowed in recent years. But this gap – which is a guide to the risk premium shares offer over bonds – still remains relatively wide by pre GFC standards.

Source: Thomson Reuters, Bloomberg, AMP Capital

And finally for real assets, using commercial property as a guide, as indicated earlier the risk premium offered by commercial property relative to bonds remains wide, albeit it has narrowed as property yields have fallen and bond yields have risen (a bit). Overall, it’s hard to argue the search for yield has gone too far given how low bond yields still are. That said, corrections like what we saw in shares and corporate debt during 2015-16 are healthy in ensuring this remains the case.

But what about the risk of an upswing in bond yields, particularly with the Fed moving to quantitative tightening? This is the biggest risk and our view is that the super cycle bull market in bonds is over. See “The end of the super cycle bull market in bonds?” which can be found at http://bit.ly/2fLoTNw. There are several reason for this:

-

First, global growth is looking stronger as evident in strong business conditions indicators across most countries. Global growth is improving and becoming more synchronised globally. Nearly 75% of the 45 countries tracked by the OECD are seeing accelerating growth, the highest it’s been since the initial bounce out of the GFC in 2010.

-

Part of the reason for this is that the “muscle memory” from the GFC, which commenced a decade ago, is fading and this is contributing to stronger confidence.

-

The risk of deflation is receding and giving way to the risk of a rise in inflation as capital and labour utilisation is on the rise globally & productivity growth is poor, reflecting: low levels of investment; increasing levels of populist regulation in some countries; and as older workers retire. While the impact of technological innovation (the Amazon effect, artificial intelligence) will keep this gradual there will still be a cycle in inflation and the risks are gradually pointing up.

-

Reflecting this, central banks are gradually retreating from ultra easy policy. The Fed is the most advanced here as the US economic recovery is further advanced. As a result, the Fed is moving towards allowing its holding of government bonds and mortgage-backed securities to start declining. This will be achieved by the Fed not rolling over (ie not reinvesting) the bonds on its books as they mature so it won’t be as dramatic as actually selling bonds. But its holding of bonds will nevertheless decline and it will be sucking cash out of the US economy. In other words, it will be undertaking “quantitative tightening” to reverse the “quantitative easing” of a few years ago. This is good news and reflects the strength of the US economy much as its commencement of rate hikes did in 2015. Nevertheless, combined with continuing gradual Fed rate hikes, it will likely see a resumption of the upwards pressure on bond yields acting as a gradual dampener on the search for yield.

The upswing in bond yields is likely to be gradual – with periodic spurts higher then fall backs like over the last year – as the Fed will likely be gradual, other central banks including the Reserve Bank of Australia are well behind the Fed in being able to tighten and yield focussed demand from aging populations will act as a constraint. But the trend in bond yields is likely to be up unless there is an unexpected relapse in global growth.

What does it all mean for investors?

There are several implications for investors: expect lower returns from government bonds as yields gradually rise; the search for yield likely has further to go in relation to commercial property and infrastructure but it is likely to wane as bond yields rise; share markets are now more dependent on earnings growth for future gains (and the signs are positive) but cyclical sectors geared to higher earnings will likely be the outperformers and yield plays may be underperformers. That the Fed is moving to start reversing its post-GFC quantitative easing (money printing) is another sign the global economy is getting back to normal. This is good for investors.

Source: AMP Capital 21 September 2017

Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.