Two years after it first started raising interest rates in this cycle in December 2015, the Fed has increased rates for the fifth time, raising the Fed Funds rate another 0.25% to a target range of 1.25-1.5%. For the last two years, it has been right not to fear the Fed as tightening was conditional on better economic conditions, it would be gradual and we were only moving from very easy monetary policy to less easy. Despite a few ructions after the first move into early last year, this has been correct as the US and global recovery has accelerated and share markets and other growth assets have performed well. The question now is where to from here? Will the Fed get more aggressive? Should investors be more concerned?

Fed hike number 5

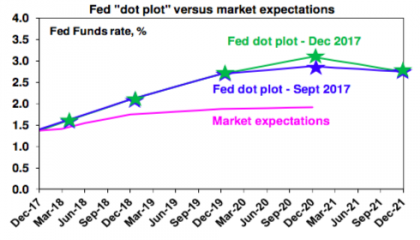

In raising the target range for the Fed Funds rate by another 0.25%, the Fed noted the continuing strengthening in the US labour market and solid growth and continues to expect inflation to pick up towards its 2% target. The Fed continues to refer to only “gradual” increases in interest rates going forward and the Fed’s so-called “dot plot” median of Fed meeting participants’ interest rate expectations is continuing to allow for three hikes in 2018 (the same as flagged in the September meeting). Quite clearly the Fed is confident that growth will remain strong with tax cuts providing an additional stimulus – it revised up its 2018 growth forecast from 2.1% to 2.5% – and that this will start pushing inflation back towards the 2% target.

The transition to new leadership at the Fed in March from Janet Yellen to Jerome Powell (assuming he is confirmed by the Senate, which is most likely) isn’t expected to signal a big change at the Fed on monetary policy. Powell is likely to follow the broad path the Fed is already on in terms of rates hikes and quantitative tightening. There may be a more relaxed approach to regulation, though, but for now that’s a separate issue.

Market expectations for just two Fed rates in 2018 hikes remain below the Fed’s dot plot signal of three hikes. While the market has been right in expecting lower interest rates than the Fed has been signalling in recent years, it wrongly underestimated the Fed in 2017 and is likely to do so again 2018. I suspect that the risks for US inflation are now swinging to the upside with spare capacity in the US economy gradually diminishing. So just as the market proved too cautious in allowing for just two Fed hikes this year when it has actually done three, we suspect it will be surprised again next year. In fact, given our views of a pick-up in inflation risks, we are allowing for four rate hikes next year in 2018 (conditional on tax reform being passed).

Source: US Federal Reserve, AMP Capital

Will the Fed start to become a problem for markets?

It’s still too early to get too concerned about the Fed.

-

First, the Fed is only tightening because the US economy is strong. Confidence is high, business investment is improving, the labour market is tight and profits are strong. And future rate increases will remain conditional on the economy continuing to improve.

Source: Bloomberg, AMP Capital

-

Second, for now at least, Fed rate hikes can remain “gradual” as there is still some slack remaining and inflation is currently still low.

-

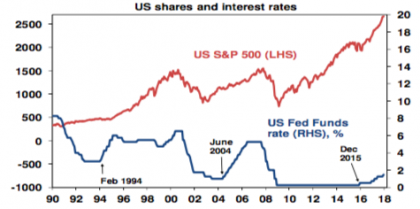

Third, US economic downturns have historically only come three years after the first Fed rate hike in a tightening cycle. And it’s likely to be even longer this time as it’s only when monetary policy becomes tight after numerous hikes that the economy gets hit and we are still a long way from that – so the gradual nature of the rate hikes so far could stretch it out further. In the last tightening cycle in 2004-2006, rates rose 17 times in just over two years – now they have only gone up five times over two years and from a much easier base. Shares often have wobbles around the first rate hike – as we saw in second half 2015 and early 2016 – but again, sustained problems usually only set in when monetary policy has become tight. This can be seen in the next chart. Shares had wobbles when interest rates first started to move up in February 1994 and in June 2004. Thereafter they resumed their rising trends and bear markets did not set in till 2000 and 2007 after multiple hikes and with recessions looming. Again, we are a long way from that.

Source: Bloomberg, AMP Capital

-

Finally, other major countries – Europe, Japan and Australia – are a long way from monetary tightening. So global monetary conditions remain very easy.

However, we are now two years into tightening and the Fed might cause a few gyrations in the year ahead.

-

The risks around inflation in the US are rising. The US labour market is even tighter than it was a year ago with most indicators pointing to very tight conditions – unemployment near 4%, ultra-low jobless claims, very high hiring and quits rates, business surveys indicating high employment plans, etc – and anecdotal evidence continuing to point to rising wages. Sooner or later this will show in higher official wage data with some flow on to inflation. Upstream price pressures are also building, which is evident in a rise in core producer price inflation from just 0.3% year on year two years ago to 2.4% now.

-

The US money market remains relatively complacent factoring less rate hikes than the Fed is signalling even though the Fed was right in 2017. This suggests the risk of a snap up in market Fed expectations at some point, particularly if inflation does start to rise as we expect.

-

The US is now further into monetary tightening so policy is no longer ultra easy. This is evident in a flattening in the US yield curve (although this may be heavily due to quantitative easing in Europe holding down Eurozone bond yields and this weighing in US bond yields).

-

Finally, after a pause this year market positioning is no longer long the US and a more aggressive Fed could see the US dollar head higher in 2018 constraining US profits, commodity prices and reigniting concerns about a dollar funding crisis in the emerging world.

So while we are not particularly concerned about the Fed, there is a case to be a bit more cautious regarding it than was the case over the last two years.

What does it mean for investors?

There are several implications for investors:

-

It’s too early for US monetary tightening to be a cyclical negative for shares, which will also likely benefit from US fiscal stimulus next year. However, the Fed is likely to become a source of volatility as next year progresses if US inflation starts to pick up as we expect. Other markets remain more attractive than US shares – notably Eurozone and Japanese shares that will benefit from cheaper valuations, easier monetary policy and lower currencies.

-

Continuing Fed rate hikes and US fiscal stimulus in 2017 will likely be a source of upwards pressure on global bond yields in 2018. So bonds are likely to continue to provide constrained returns. With the Reserve Bank of Australia (RBA) unlikely to follow the Fed though until maybe 2018, we continue to favour Australian over US bonds.

Impact on Australia

To the extent that the Fed’s further interest rate hike signals ongoing strength in the US, it’s good for Australia. It doesn’t signal that the RBA will soon follow and hike soon, though. Recent experience with the RBA hiking in 2009-10 (despite the Fed on hold at zero) and the RBA cutting in 2016 (when the Fed was hiking) highlights there is no automatic link. With the Australian economy remaining weaker relative to its potential than the US, risks around the Australian consumer, inflation running below target and Sydney and Melbourne house prices cooling, we remain of the view that the RBA will be on hold through much of next year and won’t raise rates till year end.

The main relevance of ongoing US monetary tightening is that it will serve to keep the $A down, notwithstanding the risks of a short term bounce higher in the $A. With the RBA on hold and the Fed set to continue raising rates, by March next year the Fed Funds rate will likely exceed the RBA’s cash rate with the interest rate differential set to further deteriorate against Australia through next year. If history is any guide, this is likely to see downwards pressure on the $A. We see the $A falling to around $US0.70 by end 2018 after its surprise strength in 2017.

Source: Bloomberg, AMP Capital

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.